I noticed the information in regards to the new FHFA lending price construction for Freddie Mac and Fannie Mae and thought, as traditional, issues had been being blown out of proportion. Then I noticed the desk for the brand new charges and I couldn’t imagine how they’ve made it costlier for high-down-payment debtors than low-down-payment debtors. I don’t imply the charges decreased for low down cost mortgages and are nearer, however nonetheless decrease than excessive down cost mortgages. The entire LLPA charges are decrease throughout the board for many who put 5% down or lower than those that put 20 % down.

What are FHFA and LLPA Charges?

LLPA stands for mortgage stage pricing adjustment. They’re charges that had been put in place after the 2008 crash to assist Freddie and Fannie Mae keep solvent throughout one other downturn. The Charges are utilized on most typical mortgages and had been set excessive for low down cost and low credit score debtors as a result of these debtors usually tend to default. If the charges are greater the banks will sometimes increase the rate of interest on these loans. Prior to now, folks with excessive credit score and excessive down funds paid decrease charges and had decrease rates of interest.

FHFA is the Federal Housing Finance Administration. FHFA introduced that they modified the price construction in April and has acquired a ton of backsplash after many sources claimed mortgages for top credit score and excessive down cost debtors could be costlier than mortgages for low credit score and low down cost debtors. This isn’t precisely true in all circumstances, however it’s true that the rate of interest will probably be greater for some folks with greater credit score and better down funds than these with decrease credit score and down funds.

Why did FHFA change the price construction?

FHFA stated:

“It had been a few years since a complete assessment of the Enterprises’ pricing framework was performed. FHFA launched such a assessment in 2021. The aims had been to take care of help for buy debtors restricted by earnings or wealth, guarantee a stage enjoying discipline for giant and small lenders, foster capital accumulation on the Enterprises, and obtain commercially viable returns on capital over time.”

From: https://www.fhfa.gov/Media/PublicAffairs/Pages/Assertion-from-FHFA-Director-Sandra-Thompson-on-Mortgage-Pricing.aspx

There have been different articles which have claimed race inequality was a part of the explanations for the change, however the simply of it’s, they needed to make it cheaper for low-income and low-credit rating debtors to purchase homes.

FHFA officers have justified this transfer by saying:

“An FHFA official advised The Publish the company was “tasked with making certain [Fannie and Freddie] fulfill their function in any market situation,” including that shifts in long-term mortgage charges are a far larger think about figuring out finance situations within the US housing market.

The most recent recalibration to the pricing framework that FHFA introduced in January 2023 is minimal, by comparability, and maintains market stability,” the FHFA official stated in a press release.”

That is from a New York Publish article: https://nypost.com/2023/04/16/how-the-us-is-subsidizing-high-risk-homebuyers-at-the-cost-of-those-with-good-credit/

What they stated was that rates of interest went up a ton, so that you shouldn’t fear about what we’re doing. Fear about rates of interest as a substitute.

How way more will good credit score consumers pay for a mortgage?

Whereas some consumers getting a mortgage can pay lower than earlier than, total the charges will probably be greater now. The folks paying the very best charges will probably be these with excessive down funds and low credit score. That’s proper. I stated excessive down funds. Some excessive down cost debtors with good credit score will now pay a .2 to .3% greater rate of interest than they paid earlier than. In truth, these excessive down cost debtors are paying greater charges than these placing much less cash down! Whereas excessive credit score, low down cost debtors, could also be paying decrease charges than earlier than.

On a $400,000 mortgage, a borrower with good credit score placing 20% down might pay $40 extra a month due to the upper charges. That isn’t an enormous quantity however it’s robust to bear with rates of interest already 2 to three occasions greater than 18 months in the past.

How a lot much less will spotty credit consumers pay for a mortgage?

These with decrease credit score and a excessive down cost will probably be paying lower than earlier than, however these with low credit score and a low down cost get the most important low cost. A few of the worst consumers will now get a .4% low cost on their rate of interest in comparison with what they’re paying now. These low-credit debtors gained’t be paying lower than high-credit, high-down-payment debtors, however the hole shrunk considerably.

For somebody with a 620 credit score rating and 5% down or much less, they are going to now save about $80 to $100 off their mortgage cost because of the rate of interest lower.

All consumers will now pay extra LLPA charges for 20% down vs 5% down or much less

The loopy a part of these adjustments is that throughout the board for good credit score or spotty credit, all consumers will probably be paying much less LLPA charges for having a decrease down cost (except they put greater than 25% down). Somebody with an 800 credit score rating can pay thrice the charges when placing 20% down versus placing 5% down or much less. Even somebody with a 620 credit score rating can pay much less LLPA charges when placing lower than 5% down verse 20% down.

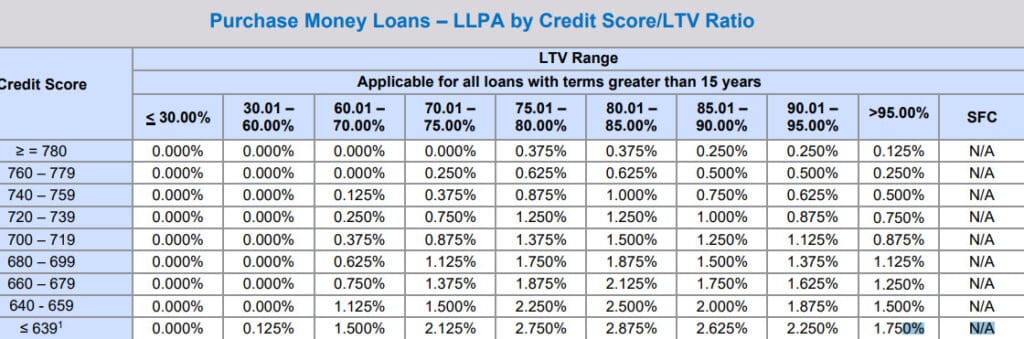

Under is the desk displaying the brand new charges:

That is from: https://singlefamily.fanniemae.com/media/9391/show

The left facet of the desk reveals the credit score scores and the highest reveals the loan-to-value ratio (the upper the quantity the much less cash persons are placing down). There are additionally many different elements that can influence these charges like debt-to-income ratios, sort of property, refinance vs new buy, and so on. The video beneath goes over the adjustments intimately.

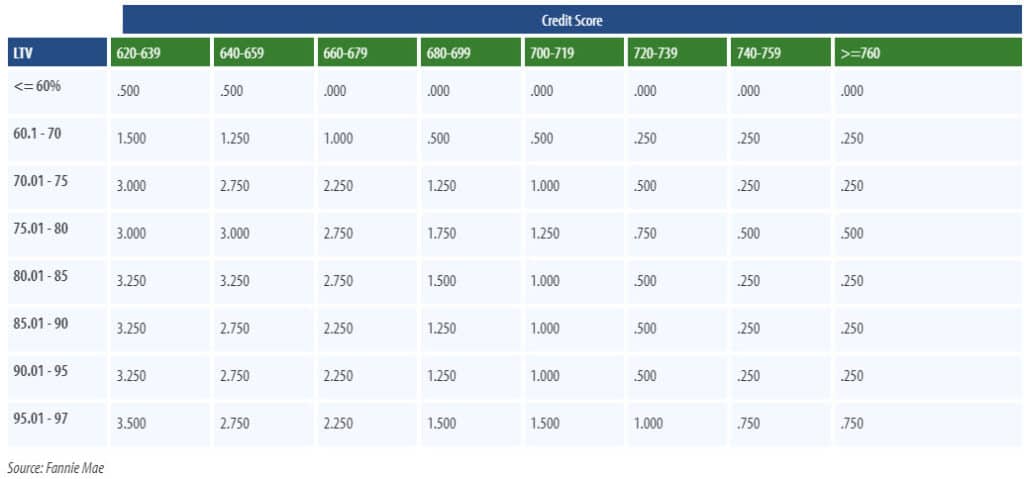

Had been the FHFA LLPA charges at all times structured to reward low-down funds?

I’m at all times skeptical of headlines and loopy tales like this. A lot of you in all probability suppose it has at all times been this manner, however the previous charges had been structured a lot otherwise. You may see them beneath:

This chart is from 2020 and could be discovered at: https://www.freeandclear.com/guides/mortgage-topics/loan-level-price-adjustments.html

As you possibly can see, the charges had been greater for low down funds and decrease for top down funds. The charges had been additionally greater for decrease credit score and low down funds. I feel widespread sense tells us that is what the chart ought to appear to be.

Do excessive down cost debtors actually pay extra?

FHFA stated in a press release that whereas the charges from FHFA for top down funds are greater than the low down funds, that doesn’t imply these excessive down cost debtors can pay extra. If you happen to put lower than 20% down on a mortgage you almost certainly will probably be paying mortgage insurance coverage which might be greater than the LLPA charges. So those that put greater than 20% down, will nonetheless almost definitely pay fewer charges. Those that put 15% or 10% down, will nonetheless have mortgage insurance coverage and have greater charges and mortgage insurance coverage than these placing 5% or much less down.

What the spokesman for FHFA didn’t point out is you can typically get mortgage insurance coverage eliminated after a few years on typical mortgages. After the mortgage insurance coverage is eliminated, many consumers who put much less down could be paying a decrease charge with out mortgage insurance coverage than those that put 20% down.

What is likely one of the craziest situations with LLPA charges?

The Mortgage Curiosity Fee Is now decrease for somebody with a 680 credit score rating placing 3% down than for somebody with a 730 credit score rating placing 15% down. If you happen to have a look at the chart from FHFA, an individual with a 730 credit score rating placing 15% down would have a 1.25% LLPA price, and the particular person with a 680 credit score rating with 3% down would pay a 1.125% price. Each of these consumers would pay mortgage insurance coverage.

Conclusion

I couldn’t imagine the numbers after I noticed them on the LLPA price desk. The media was not overblowing what had occurred, actually, I feel they missed how dangerous it was. These pointers don’t apply to FHA, VA, or USDA however for Freddie Mac and Fannie Mae. Most individuals with good credit score and debt-to-income ratios will probably be utilizing Fanie Mae and Freddie Mac and are being punished for placing extra money down.